When it comes to taxes, not all income is created equal. The way different types of income are taxed can significantly impact your overall financial health and strategy. In this post, we’ll explore how regular income is taxed marginally, the advantages of capital gains, and delve into other income types such as rental and business income. Finally, we’ll discuss how you can leverage this information for your financial advantage.

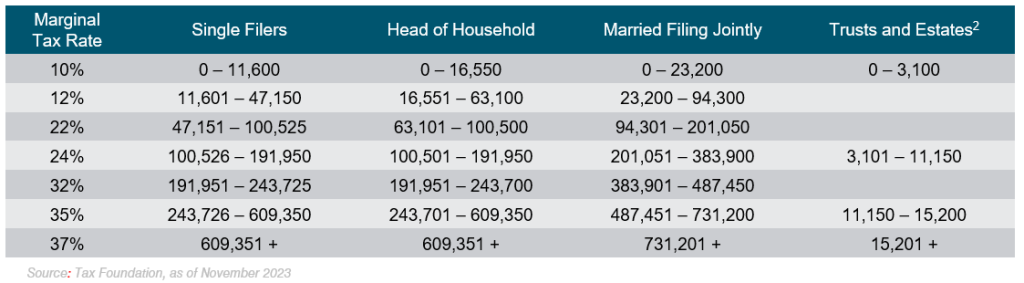

Firstly I want to point out that there is regular income and irregular income. Regular income is what you get from a W2, and is taxed as follows:

Now it is important to note the standard deduction for 2024 is 14,600 for single filers. Meaning if you make less than $14,600 you owe no federal taxes and for everyone else you owe no federal taxes on the first $14,600 you make.

For Example If you earn $50,000 a year, and are single, you will pay:

– 0% on $14,600

– 10% on the income between $14,600 and $26,200

– 12% on the remaining income between $26,201 and $50,000

This marginal tax system is designed to ensure that those who earn more contribute a higher percentage of their income, However, it can feel at times that it is punishing us for working harder.

This brings us to irregular income, income that is taxed using different rules than above.

Irregular income includes, Capital Gains, Rental, Farm and Business Income.

Capital gains refer to the profit made from selling an asset that has increased in value over time. This can include stocks, real estate, and other investments. One of the primary advantages of capital gains is that they are taxed at a lower rate if held for more than one year, if you buy and sell in the same year it is considered ordinary income. In the U.S, for instance, long-term capital gains are taxed at rates of 0%, 15%, or 20%, depending on your income level.

When it comes to rental income and business income, the tax implications can vary significantly:

The gist is, you still use the tax brackets friom ordinary income but you can now deduct expenses.

– **Rental Income:** Income earned from renting out property is generally considered passive income. It is subject to ordinary income tax rates, but landlords can deduct many expenses related to property management, such as repairs, maintenance, and depreciation. This can effectively reduce the taxable income generated from the property.

– **Business Income:** Income generated from a business is also taxed at ordinary income rates. However, business owners can take advantage of various deductions (e.g., for business expenses, equipment purchases, and employee wages) that can lower their overall taxable income. Additionally, if structured as an S-Corp or LLC, business owners may benefit from pass-through taxation, avoiding double taxation on corporate income. For S corps specifically owners may be able to save on payroll taxes.

Strategies to Take Advantage of Tax Differentials

1. Hold stocks long term

2. **Maximize Deductions:** For rental and business income, ensure you take full advantage of all available deductions. Keep meticulous records of expenses related to property management or business operations. Consult with a tax professional to identify any deductions you might be overlooking. **Consider Tax-Advantaged Accounts:** Utilize accounts such as IRAs or 401(k)s to invest for retirement. Contributions to these accounts can grow tax-deferred or even tax-free in the case of Roth accounts, allowing your investments to compound without immediate tax implications4. **Portfolio Diversification:**

5. **Utilize Tax-Loss Harvesting:** If you have investments that are underperforming, consider selling them at a loss to offset capital gains from other investments. This strategy can help reduce your tax bill while allowing you to move capital into a better investment.

6. **Leverage Passive Income Opportunities:** Look for opportunities to generate passive income, such as through rental properties or dividend-paying stocks. This income can provide cash flow while offering potential tax benefits.

7. **Stay Informed:** Tax laws often change, and new opportunities savings can arise. Stay informed about current tax legislation and consider consulting with a tax professional to strategize your income sources.

Navigating the complexities of income taxation can be daunting, for the best strategies, and solutions to your problem schedule a consultation with tactics.tax. And remember, not all income is created equal, and with the right approach, you can take advantage of these differences to build a more prosperous future.